Lemon and orange updates

Mixed conditions for lemon and orange crops.

Lemon prices increased notably in May, but generally remain at or below profitable levels. Harvest in the Coastal growing region is progressing well and quality is reportedly good. The size profile appears to be larger than average overall. Imports from Argentina and Chile are expected to increase over the coming weeks. The World Citrus Organization forecasts production in the Southern Hemisphere will decrease 2.36% in 2026. This may be in part due to increased fuel and fertilizer costs resulting from the ongoing blockade of the Strait of Hormuz. A smaller global lemon crop could be supportive of prices next season.

Navel harvest is nearing the end for the season and while prices jumped earlier in the month, they remain well below last season. Harvest on the Valencia crop is getting underway and early reports suggest generally strong quality and utilization rates (the percentage of fruit going to fresh markets). Initial estimates suggest Brazil’s orange crop will decline 13% year over year due to challenging weather conditions, reduced inputs due to rising costs, and citrus greening disease. (Brazil is the largest supplier of oranges for frozen concentrate.) A smaller crop may be supportive of orange and orange juice prices.

Profitability

June 10, 2026Lemons: Breakeven profitability - Neutral 12-month outlook

Oranges: Slightly profitable - Neutral 12-month outlook

Relatively weak market conditions will continue to pressure lemon prices.

Relatively strong markets along with fruit supply and quality are supportive of prices.

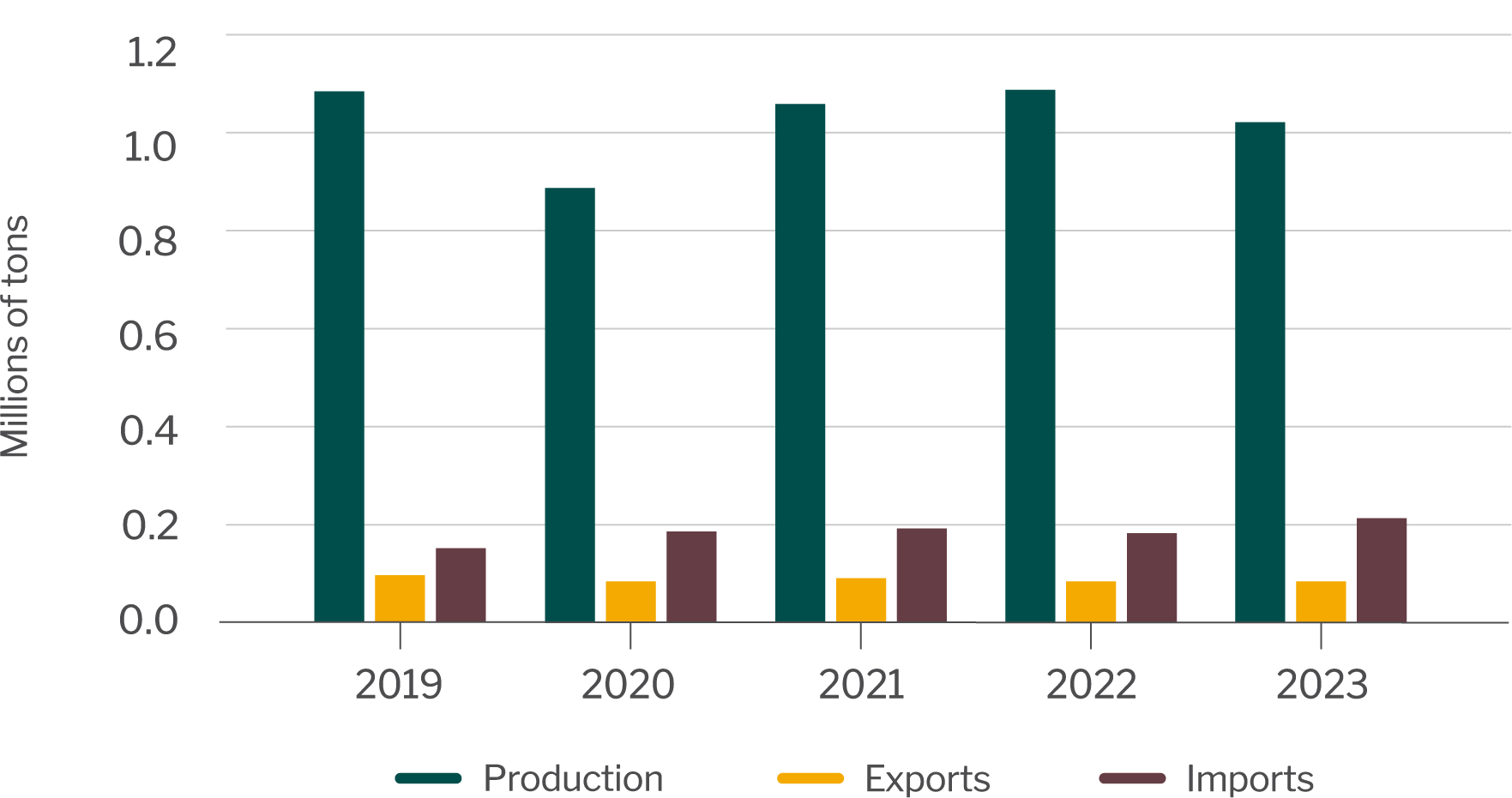

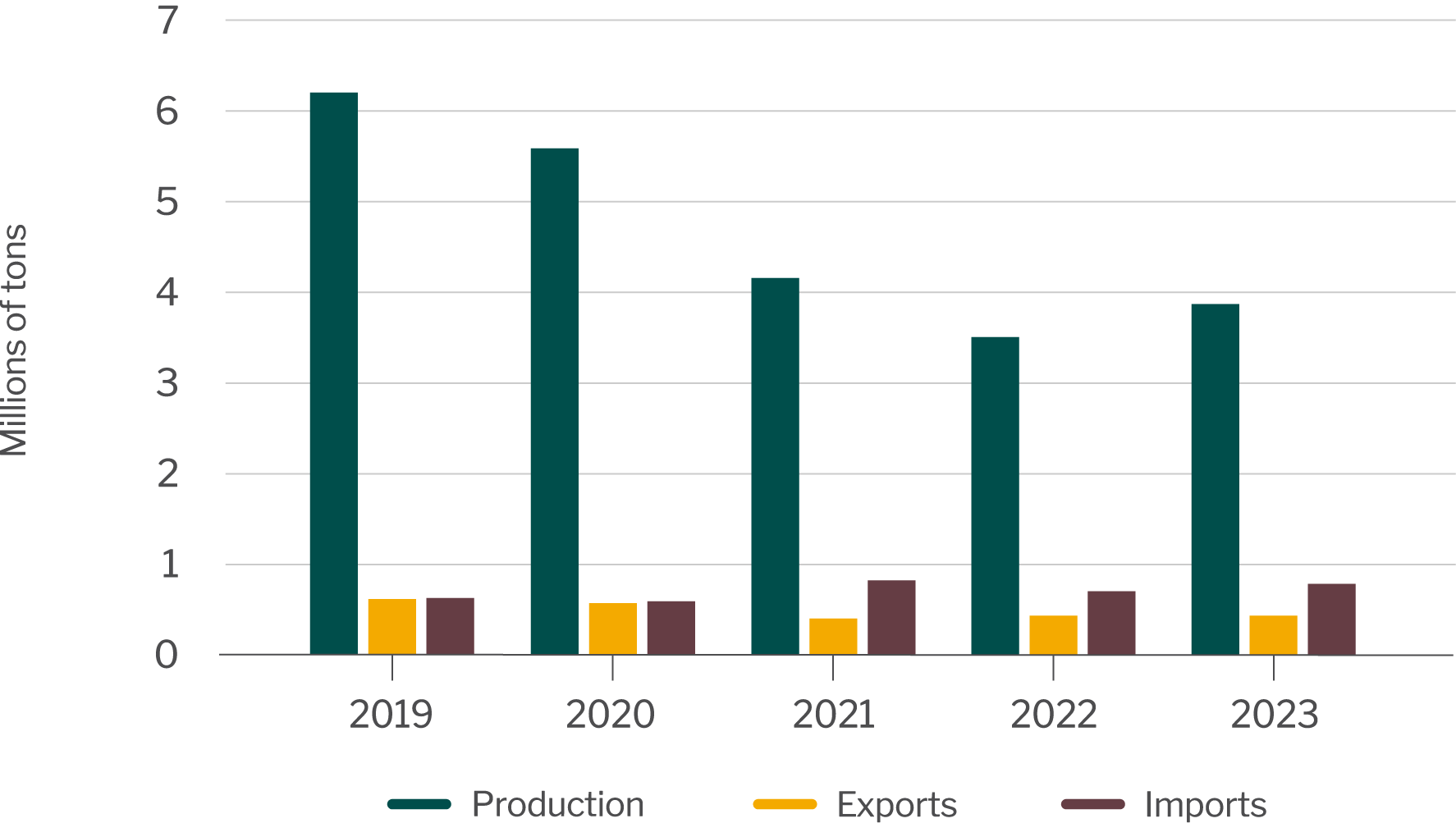

Domestic markets make up the vast majority of lemon and orange demand, with exports only accounting for about 11% of total production. The largest foreign markets include Canada, South Korea, Mexico, Japan, and to a much lesser extent, Hong Kong. Lemon and orange imports have increased significantly over the last decade and make up 17% of total domestic supply, a relatively high amount compared to other specialty crops. Increased plantings coupled with low labor costs and minimal trade barriers have enabled citrus growers in Central and South America to compete in U.S. markets.

Lemon production, exports and imports

USDA Citrus Fruits Summary. U.S. Census Bureau. Crop year is from August to July.

Orange production, exports and imports

USDA Citrus Fruits Summary. U.S. Census Bureau. Crop year is from October to September.

Tariff tracker - Tariff rates applied to U.S. trade partners are consistenly updated to reflect policy changes. The World Trade Organization (WTO) tracks duties and tariffs on lemons and oranges. For your convenience, the following links will take you to tariff data for South Korea (fresh oranges and mandarins/tangerines/satsumas) and Japan (fresh oranges and mandarins/tangerines/satsumas). Citrus fruits are currently exempt from tariffs with Canada under the United States-Mexico-Canada Agreement (USMCA), but please refer to the U.S. Trade Representative website for up-to-date information. WTO also tracks rates for lemon imports and orange imports to the U.S. Please consult with a trade lawyer or professional for detailed and up-to-date insights on tariff rates and their application to lemons and oranges.

For guidance on interpreting duty and tariff rates, please refer to our Tariff Guide.

Lemon and orange updates

Mixed conditions for lemon and orange crops.

Lemon prices increased notably in May, but generally remain at or below profitable levels. Harvest in the Coastal growing region is progressing well and quality is reportedly good. The size profile appears to be larger than average overall. Imports from Argentina and Chile are expected to increase over the coming weeks. The World Citrus Organization forecasts production in the Southern Hemisphere will decrease 2.36% in 2026. This may be in part due to increased fuel and fertilizer costs resulting from the ongoing blockade of the Strait of Hormuz. A smaller global lemon crop could be supportive of prices next season.

Navel harvest is nearing the end for the season and while prices jumped earlier in the month, they remain well below last season. Harvest on the Valencia crop is getting underway and early reports suggest generally strong quality and utilization rates (the percentage of fruit going to fresh markets). Initial estimates suggest Brazil’s orange crop will decline 13% year over year due to challenging weather conditions, reduced inputs due to rising costs, and citrus greening disease. (Brazil is the largest supplier of oranges for frozen concentrate.) A smaller crop may be supportive of orange and orange juice prices.

Profitability

June 10, 2026Lemons: Breakeven profitability - Neutral 12-month outlook

Oranges: Slightly profitable - Neutral 12-month outlook

Relatively weak market conditions will continue to pressure lemon prices.

Relatively strong markets along with fruit supply and quality are supportive of prices.

Domestic markets make up the vast majority of lemon and orange demand, with exports only accounting for about 11% of total production. The largest foreign markets include Canada, South Korea, Mexico, Japan, and to a much lesser extent, Hong Kong. Lemon and orange imports have increased significantly over the last decade and make up 17% of total domestic supply, a relatively high amount compared to other specialty crops. Increased plantings coupled with low labor costs and minimal trade barriers have enabled citrus growers in Central and South America to compete in U.S. markets.

Lemon production, exports and imports

USDA Citrus Fruits Summary. U.S. Census Bureau. Crop year is from August to July.

Orange production, exports and imports

USDA Citrus Fruits Summary. U.S. Census Bureau. Crop year is from October to September.

Tariff tracker - Tariff rates applied to U.S. trade partners are consistenly updated to reflect policy changes. The World Trade Organization (WTO) tracks duties and tariffs on lemons and oranges. For your convenience, the following links will take you to tariff data for South Korea (fresh oranges and mandarins/tangerines/satsumas) and Japan (fresh oranges and mandarins/tangerines/satsumas). Citrus fruits are currently exempt from tariffs with Canada under the United States-Mexico-Canada Agreement (USMCA), but please refer to the U.S. Trade Representative website for up-to-date information. WTO also tracks rates for lemon imports and orange imports to the U.S. Please consult with a trade lawyer or professional for detailed and up-to-date insights on tariff rates and their application to lemons and oranges.

For guidance on interpreting duty and tariff rates, please refer to our Tariff Guide.

IN THIS SECTION

![]()

Lemon and Orange Industry Perspective

View the latest AgWest Lemon and Orange Industry Perspective.

Learn more