Cattle updates

Drought challenges an otherwise strong market.

Strong cattle prices continue to support cow-calf profitability, but drought and water shortages are increasing production risks across the West. Cow-calf producers throughout AgWest's territory continue to benefit from historically strong cattle markets, with national steer calf prices up 24% year over year in mid-June and AgWest states averaging even stronger gains of 28%. In Montana, fall calf contracts reportedly reached $2,800 to $3,150 per head, reflecting tight cattle supplies and resilient beef demand. However, producers face headwinds with 70% of Arizona pasture and 38% of Montana pasture rated poor or very poor. These conditions are tightening forage supplies, prompting many cattle producers to secure hay supplies ahead of fall.

Margin pressure is increasing across the cattle supply chain as historically high feeder cattle prices and shrinking cattle supplies shape market dynamics. Feedlot operators and backgrounders are paying record prices to procure cattle, leading buyers to become more selective with placements and making risk management increasingly important to protect margins. At the same time, packers’ profitability is struggling in the current market. Packers are beginning to reduce slaughter capacity to better align with tighter cattle supplies. This is highlighted by JBS's planned closure of beef processing facilities in Pennsylvania and Tennessee. Reduced processing capacity and fewer active buyers could lessen competition for cattle.

New World screwworm remains a closely monitored animal health issue, though market impacts have been limited thus far. The first U.S. case was confirmed on June 3 in Texas along the Mexican border. Confirmed cases increased to 29 by June 30 and the disease also surfaced in New Mexico. Cattle futures markets responded bearishly, but price impacts were short-lived. Currently the largest risks for cattle producers stem from market uncertainty and consumer perception rather than widespread livestock losses. USDA continues to focus on targeted quarantines and sterile fly releases as part of its eradication and containment strategy. States are also taking proactive steps to strengthen biosecurity measures and limit the spread of animal diseases. In Idaho, health certificates are required for all livestock and domestic pets entering the state. Additionally, Idaho has implemented restrictions prohibiting the entry of livestock originating from or transiting through Mexico, regardless of health certification status or method of transportation.

Profitability

June 10, 2026Cattle feeders: Slightly profitable - Neutral 12-month outlook

Cow-calf producers: Very profitable - Neutral 12-month outlook

Strong fed cattle prices and heavy carcass weights have helped offset higher feeder cattle costs.

Record-high calf prices, driven by historically tight cattle supplies and strong beef demand, have more than offset elevated production costs.

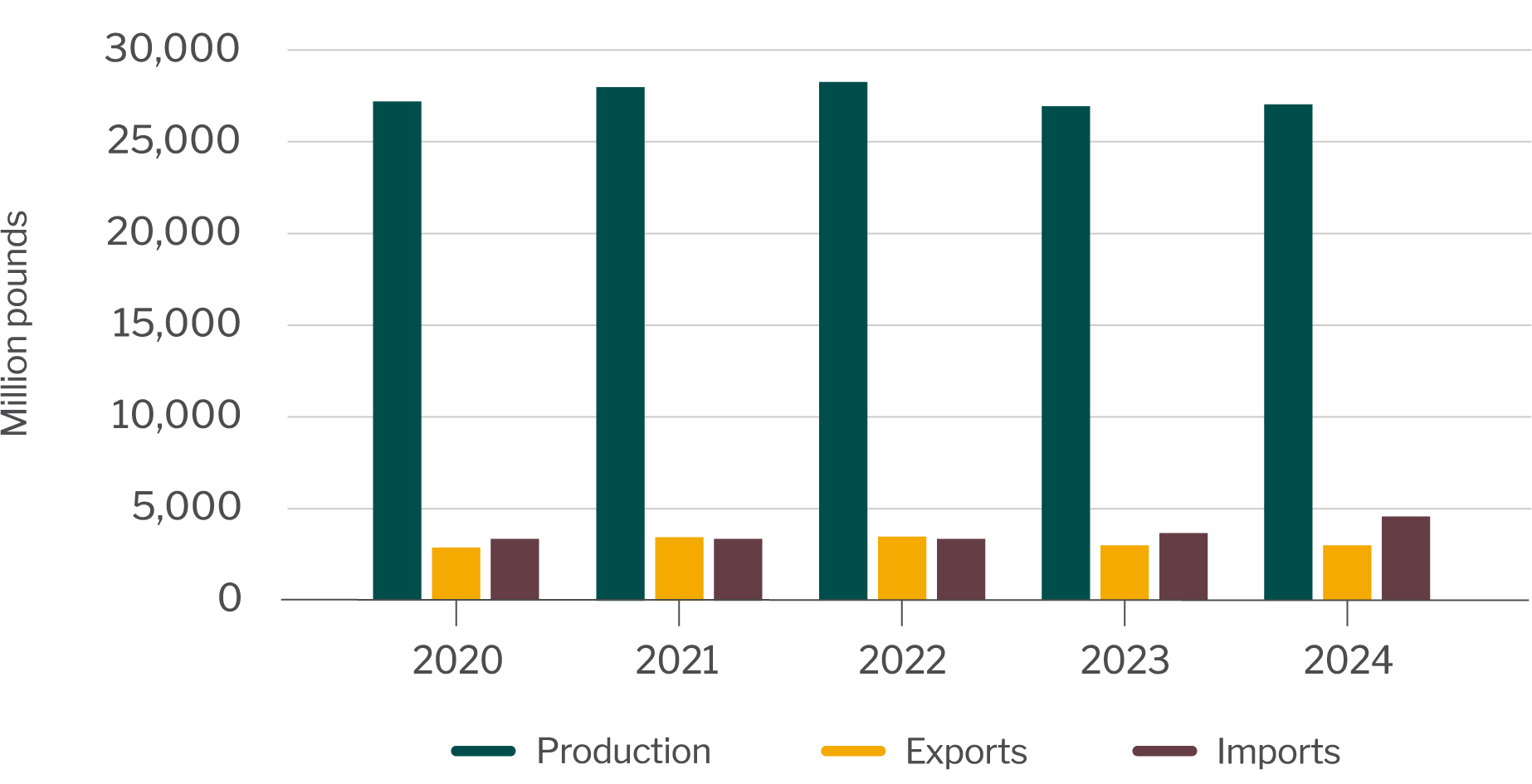

Exports play a key role in driving demand for U.S. beef, with 12% of production exported. Major export destinations include Japan, South Korea, China, Mexico and Canada. Exports also increase the value of beef byproducts, including variety meats (e.g., tongue, cheek meat, hearts) along with tallow and hides, which have limited demand domestically. The higher prices and increased sales of these items boost overall live cattle values and improve packers' margins.

Beef imports primarily consist of lean processing beef used in ground beef to meet domestic consumer demand. Over the past decade, U.S. imports of fresh or chilled beef have more than doubled. Given the tight domestic cattle supply, beef imports are important to meeting consumer demand for beef.

Beef production, exports and imports

USDA Livestock and Meat International Trade Data.

Tariff tracker - Tariff rates applied to U.S. trade partners are consistenly updated to reflect policy changes. The World Trade Organization (WTO) tracks duties and tariffs on beef products and live cattle by country. For your convenience, the following links will take you to tariff data on fresh or chilled bovine meat (a leading U.S. export for the cattle industry) for top markets including South Korea and China. Beef products are currently exempt from tariffs for Mexico and Canada under the United States-Mexico-Canada Agreement (USMCA), but please refer to the U.S. Trade Representative website for up-to-date information. WTO also tracks rates for beef imports to the U.S. Please consult with a trade lawyer or professional for detailed and up-to-date insights on tariff rates and their application to cattle.

For guidance on interpreting duty and tariff rates, please refer to our Tariff Guide.

Cattle updates

Drought challenges an otherwise strong market.

Strong cattle prices continue to support cow-calf profitability, but drought and water shortages are increasing production risks across the West. Cow-calf producers throughout AgWest's territory continue to benefit from historically strong cattle markets, with national steer calf prices up 24% year over year in mid-June and AgWest states averaging even stronger gains of 28%. In Montana, fall calf contracts reportedly reached $2,800 to $3,150 per head, reflecting tight cattle supplies and resilient beef demand. However, producers face headwinds with 70% of Arizona pasture and 38% of Montana pasture rated poor or very poor. These conditions are tightening forage supplies, prompting many cattle producers to secure hay supplies ahead of fall.

Margin pressure is increasing across the cattle supply chain as historically high feeder cattle prices and shrinking cattle supplies shape market dynamics. Feedlot operators and backgrounders are paying record prices to procure cattle, leading buyers to become more selective with placements and making risk management increasingly important to protect margins. At the same time, packers’ profitability is struggling in the current market. Packers are beginning to reduce slaughter capacity to better align with tighter cattle supplies. This is highlighted by JBS's planned closure of beef processing facilities in Pennsylvania and Tennessee. Reduced processing capacity and fewer active buyers could lessen competition for cattle.

New World screwworm remains a closely monitored animal health issue, though market impacts have been limited thus far. The first U.S. case was confirmed on June 3 in Texas along the Mexican border. Confirmed cases increased to 29 by June 30 and the disease also surfaced in New Mexico. Cattle futures markets responded bearishly, but price impacts were short-lived. Currently the largest risks for cattle producers stem from market uncertainty and consumer perception rather than widespread livestock losses. USDA continues to focus on targeted quarantines and sterile fly releases as part of its eradication and containment strategy. States are also taking proactive steps to strengthen biosecurity measures and limit the spread of animal diseases. In Idaho, health certificates are required for all livestock and domestic pets entering the state. Additionally, Idaho has implemented restrictions prohibiting the entry of livestock originating from or transiting through Mexico, regardless of health certification status or method of transportation.

Profitability

June 10, 2026Cattle feeders: Slightly profitable - Neutral 12-month outlook

Cow-calf producers: Very profitable - Neutral 12-month outlook

Strong fed cattle prices and heavy carcass weights have helped offset higher feeder cattle costs.

Record-high calf prices, driven by historically tight cattle supplies and strong beef demand, have more than offset elevated production costs.

Exports play a key role in driving demand for U.S. beef, with 12% of production exported. Major export destinations include Japan, South Korea, China, Mexico and Canada. Exports also increase the value of beef byproducts, including variety meats (e.g., tongue, cheek meat, hearts) along with tallow and hides, which have limited demand domestically. The higher prices and increased sales of these items boost overall live cattle values and improve packers' margins.

Beef imports primarily consist of lean processing beef used in ground beef to meet domestic consumer demand. Over the past decade, U.S. imports of fresh or chilled beef have more than doubled. Given the tight domestic cattle supply, beef imports are important to meeting consumer demand for beef.

Beef production, exports and imports

USDA Livestock and Meat International Trade Data.

Tariff tracker - Tariff rates applied to U.S. trade partners are consistenly updated to reflect policy changes. The World Trade Organization (WTO) tracks duties and tariffs on beef products and live cattle by country. For your convenience, the following links will take you to tariff data on fresh or chilled bovine meat (a leading U.S. export for the cattle industry) for top markets including South Korea and China. Beef products are currently exempt from tariffs for Mexico and Canada under the United States-Mexico-Canada Agreement (USMCA), but please refer to the U.S. Trade Representative website for up-to-date information. WTO also tracks rates for beef imports to the U.S. Please consult with a trade lawyer or professional for detailed and up-to-date insights on tariff rates and their application to cattle.

For guidance on interpreting duty and tariff rates, please refer to our Tariff Guide.