Quarterly Economic Update: October 2025

Executive summary

The U.S. economy continues to navigate policy changes, trade uncertainty, and evolving monetary policy. Last month, the Federal Open Market Committee (FOMC) cut the federal funds target rate range by 25 basis points to 4.00-4.25%. It was the first rate cut since the second half of last year. Despite year-over-year inflation averaging about 2.9%, recent job growth data suggested risks to employment have increased, leading to the rate cut. Policymakers remain focused on balancing inflation and employment, while businesses and consumers adjust to ongoing volatility.

Economic drivers

Tariffs and related legal battles unsettle business conditions.

The Trump administration’s tariff strategy remains a central driver of business conditions. While legal challenges to tariffs—particularly those issued under the International Emergency Economic Powers Act—are set to be reviewed by the Supreme Court, the ongoing debate has left companies facing unpredictable trade costs and regulatory risks. Recently, there has been a notable decline in business spending and investment, with many attributing this slowdown to the unsettled trade policy environment. Even as the administration explores alternative legal avenues for implementing tariffs, businesses are delaying investments and restructuring supply chains in response to shifting regulations and global tensions. Regardless of the Supreme Court’s decision, persistent legal and legislative battles are likely to keep trade policy uncertainty elevated, weighing on business confidence and economic growth.

Spending bill passes through Congress, but appropriations remain unresolved.

In July the U.S. Congress enacted the 2026 federal budget proposal, also known as the One Big Beautiful Bill Act, which was signed by President Trump. The Bill averted a $4 trillion tax hike on Americans, reformed social programs, promoted a pro-business environment and expanded state and local tax deductions. Separate from the legislation are appropriations bills, which fund day-to-day government operations. Congress failed to approve a set of resolutions ahead of the deadline, and at the writing of this report the federal government is in the process of shutting down its daily activities. This is likely to be short lived with minimal long-term impacts.

The Fed eases policy rates on weaker employment data.

Look for monetary policy to remain a primary driver of short-term interest rates over the next several months as the Federal Reserve seeks to balance risks to its dual mandate of stable prices (inflation) and full employment. Fed officials believe growth moderated in the first half of the year as job gains have slowed and the unemployment rate has edged higher. In the September policy statement released by the FOMC, policymakers indicated “downside risks to employment have risen,” while inflation “has moved up and remains somewhat elevated” compared to the Committee’s 2% target. Based on this outlook, policy rates were reduced by 25 basis points, which lowered the federal funds target range to 4.00-4.25%.

In Fed Chair Powell’s post FOMC press conference, he indicated while tariff-related inflation could be temporary, it might last longer than expected. The Fed will continue to assess the impact of executive policy when adjusting monetary policy. He also noted Committee members have diverse views on where interest rates should be given the challenges and uncertainty of the economic landscape which includes fiscal policy and trade policy.

Federal funds futures are suggesting policy rates may be eased by 25 basis points at the late-October or mid-December FOMC meetings. If upcoming employment reports signal a much weaker labor sector, the Fed may cut rates at both meetings. The market is also looking for an additional 50 basis points in rate cuts 2026. However, this outlook will greatly depend on how well the economy performs during this time, especially as it relates to the level of inflation and employment.

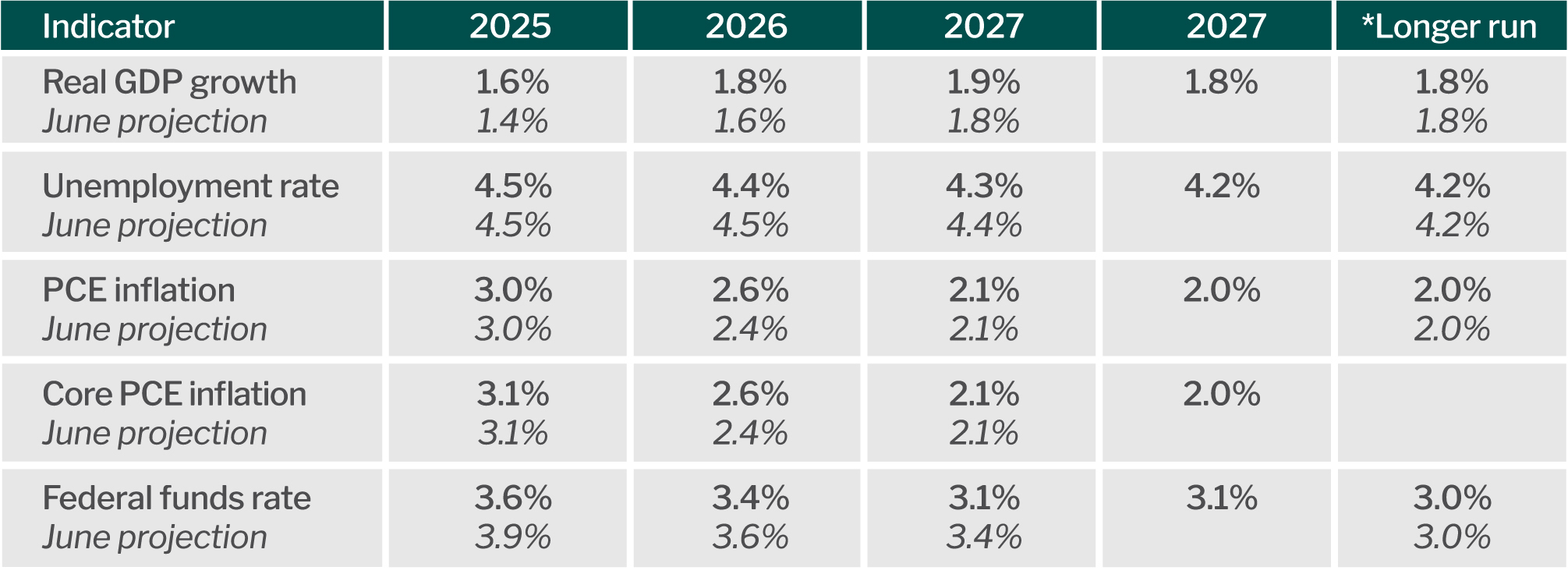

On Sept. 17, the FOMC released its latest forecast for the economy as part of its monetary policy statement.

Federal Reserve Projections as of September 2025

Source: Federal Reserve Board.

Risks to the economy

The following present risks to the economic outlook:

- A protracted government shutdown could reduce economic activity and government support services as well as impact treasury markets.

- Sustained uncertainty with tariff policy may lead to a contraction in business investments. Reduced business investment could result in lower employment levels and fewer goods and services available to consumers.

- A pending Supreme Court case may clarify the extent of presidential authority over the Federal Reserve, raising concerns about the central bank’s independence. Any erosion of Fed autonomy could have significant implications for monetary policy, financial market stability, and long-term economic growth.

- The debt to GDP ratio is now at about 118%. Rising federal debt levels could increase inflation and treasury yields, weaken the U.S. dollar and reduce the capacity of the U.S. government to respond to an economic crisis and war. Sustained growth in debt could lead to a fiscal debt crisis, and subsequently hardship for the American people.

- Rising prices and debt loads lead to greater financial stress, particularly among low wage earners who spend more of their income on essentials. Coupled with a weaker equity market and deterioration in the wealth effect, this may eventually slow consumer spending. Delinquencies for consumer credit cards and auto loans are trending higher.

Economic data and trends

Employment

Jobs, Unemployment and Hourly Earnings .jpg?sfvrsn=883464c0_1)

Source: Bureau of Labor Statistics.

Gross Domestic Product

Gross Domestic Product

Source: Bureau of Economic Analysis.

Inflation

Consumer Price Index .jpg?sfvrsn=e84708f1_1)

Source: U.S. Bureau of Labor Statistics. U.S. Bureau of Economic Analysis

Return to Industry Insights home page

IN THIS SECTION

![]()

.jpg?Status=Master&sfvrsn=68087301_1 "My project-1 (26)")

Economic headlines, data and trends

Monthly economic trends, data and major industry headlines.

Learn more