Quarterly Economic Update: July 2025

Executive summary

The threat and application of tariffs, conflict in the Middle East, progress on a spending bill in Congress and stable policy by the Federal Reserve drove economic conditions in Q2 2025. These drivers resulted in increased business uncertainty, market volatility, inflation expectations and geopolitical tensions. Treasury yield movement remains moderate, with 2-year and 10-year bonds trading in the middle of their six-month ranges at 3.87% and 4.33%, respectively. Major U.S. indices are up 5-6% year to date. While these readings suggest a stable economy heading into Q3 2025, conditions can change rapidly and investors/traders will alter their outlook and positions accordingly.

Economic drivers

Tariffs disrupt business conditions.

The threat and application of tariffs by the Trump Administration has increased geopolitical tensions with key trading partners as well as uncertainty for businesses dependent on international trade. While this may impact economic growth in the short-term, the U.S. is now actively engaged in trade negotiations to improve the competitiveness of domestic producers. Further, the prospect of stricter trade barriers has led several multinational companies to announce plans to invest within the U.S., including Texas Instrument’s $60 billion commitment to build a microchip factory. Greater manufacturing capacity could increase employment in a sector that is generally thought of as more stable and higher paying than others. Efforts to improve the competitiveness of U.S. producers are likely not finished yet and conditions will remain uncertain for the foreseeable future. Whether or not this will have a meaningful, lasting impact on the balance of trade is yet to be seen.

Tensions in the Middle East increase volatility and risk.

Energy prices surged mid-June as Israel and Iran entered into war. Israel initiated the conflict following the International Atomic Energy Agency’s (IAEA) findings that Iran is in violation of its nuclear non-proliferation obligations. Soon after, the U.S. entered directly by bombing several nuclear facilities in Iran. While a ceasefire reached on June 24 appears to be holding, conditions remain fragile and a return to violence could lead to disrupted trade flows, higher oil prices, weaker global economic growth, volatile bond and stock markets and increased geopolitical tensions with Russia and China. Nevertheless, oil prices are near the middle of their six-month trading range.

Spending bill progresses through Congress.

The debt limit was reinstated in January 2025 following a temporary suspension. At the current pace of spending, the government’s ability to borrow will be exhausted by late August or early September. The 2026 federal budget proposal, also known as the One Big Beautiful Bill Act (the Bill), passed through Congress and is set to be signed by President Trump at the writing of this report. The Bill will avert a $4 trillion tax hike on Americans, reform social programs, promote a pro-business environment and expand state and local tax deductions. The signing helps to avoid a default on U.S. Treasury debt, and thus a sharp increase in interest rates and volatility.

Fed policy remains unchanged, but markets suggest rate cuts are coming.

In June 2025, Federal Open Market Committee (FOMC) policymakers held monetary policy rates steady with the federal funds target range at 4.25%-4.50% and indicated economic activity “has continued to expand at a solid pace” while labor market conditions “remain solid.” Despite negative real Gross Domestic Product (GDP) growth for Q1-2025, officials stated uncertainty in the U.S. economic outlook has “diminished but remains elevated” compared to a few months ago, inflation is “somewhat elevated,” and maintaining a restrictive bias with monetary policy rates is appropriate at this time. Federal funds futures suggest the Fed will cut policy rates by 25 basis points in September and December, and will cut another two 25 basis points in the first half of 2026.

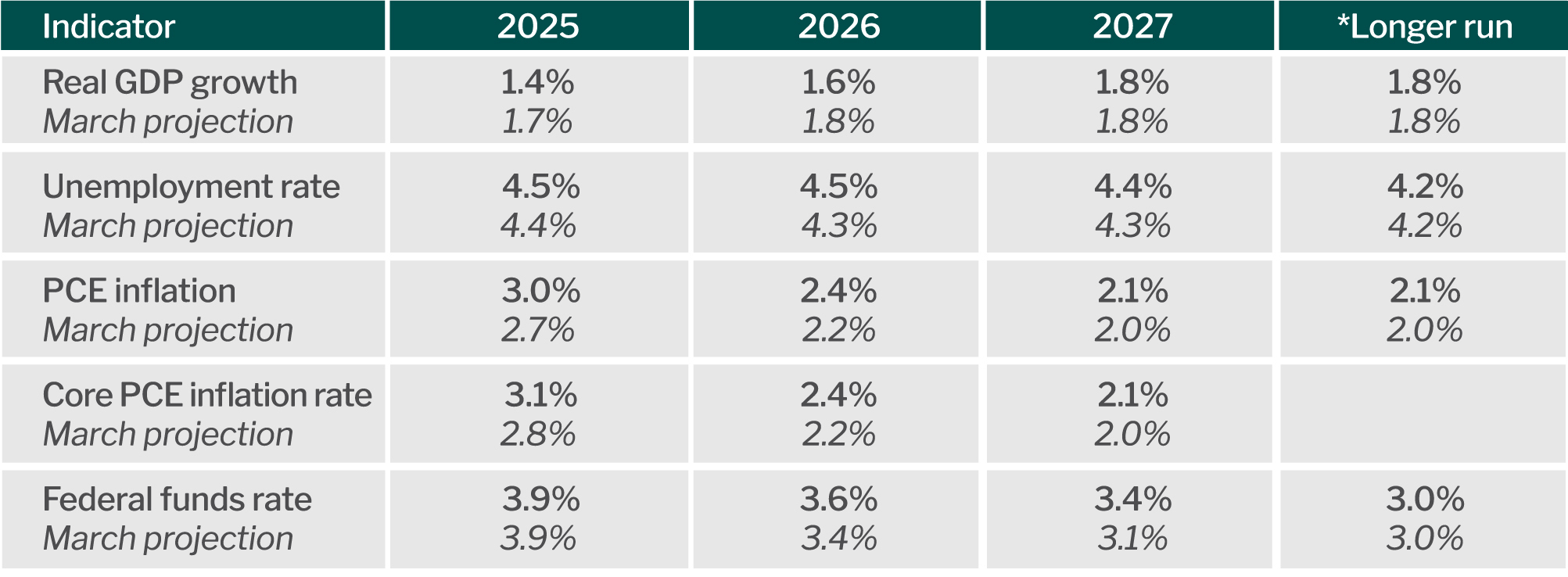

The Fed released its latest forecast for the economy as part of its monetary policy statement on June 18.

Federal Reserve Projections as of July 2025

Source: Federal Reserve Board.

Risks to the economy

The following present risks to the economic outlook:

- U.S. engagement in a protracted war with Iran could further pressure deficit spending, divert resources away from the economy, drive up oil prices, increase inflation and reduce international tourism due to security concerns.

- The Trump Administration implements policies that are inconsistent and/or disjointed, leading to an increasingly uncertain business environment.

- The debt to GDP ratio is now at about 121% and continues to grow. Rising federal debt levels could increase inflation and treasury yields, weaken the U.S. dollar and reduce the capacity of the U.S. government to respond to an economic crisis and war. Sustained growth in debt will eventually lead to an economic crisis, and subsequently hardship for the American people.

- Rising prices and debt loads lead to greater financial stress, particularly among low wage earners. Coupled with a weaker equity market and deterioration in the wealth effect, this may eventually slow consumer spending. Delinquencies for consumer credit cards and auto loans are trending higher.

Economic data and trends

Employment

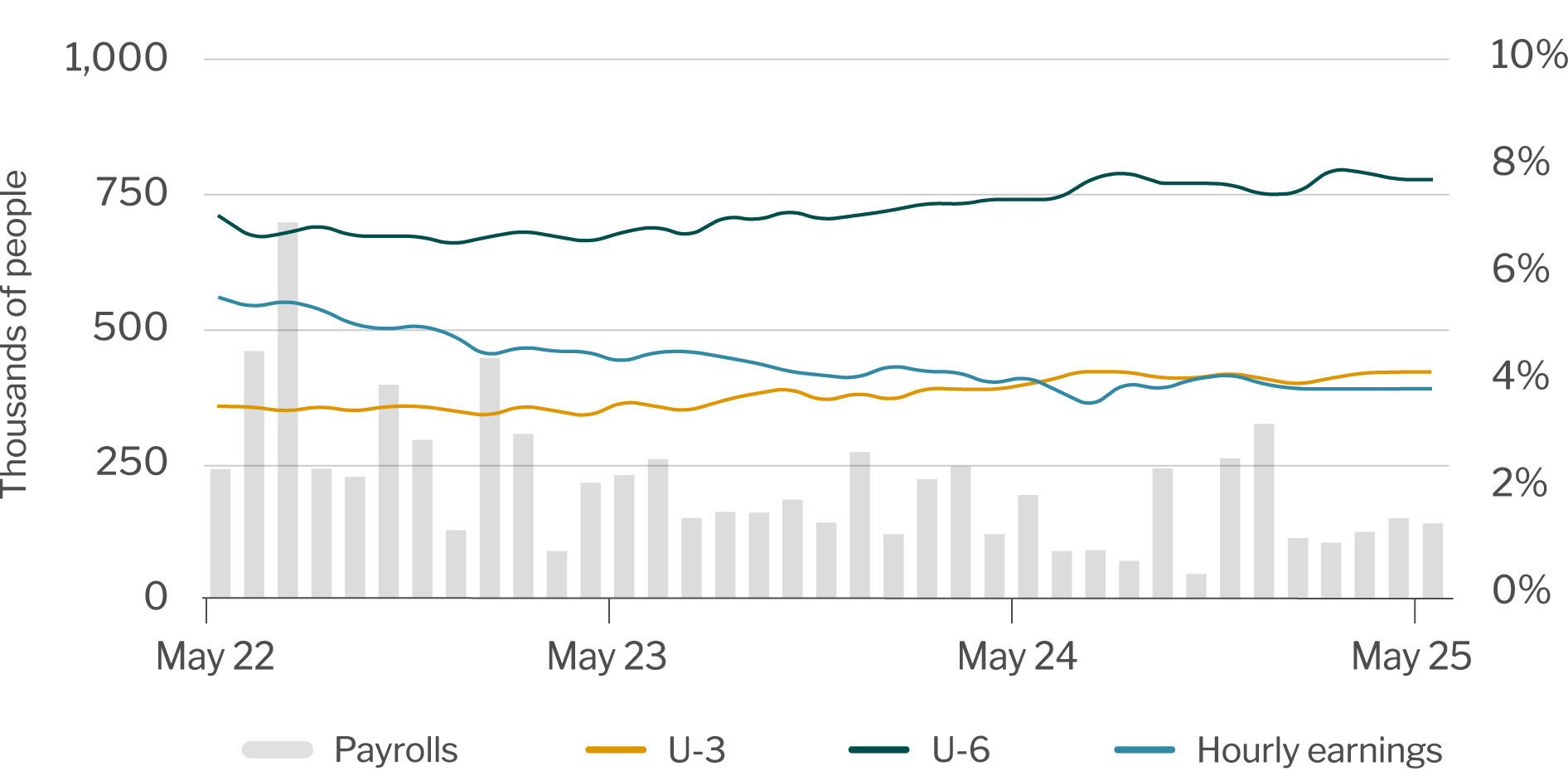

The labor sector has softened over the past six months. For June, 147,000 new nonfarm payrolls were generated while the unemployment rate decreased 0.1 percentage points to 4.1%. In 2024, monthly job gains averaged 168,000 per month, which compares to an average of 130,000 for the first six months of 2025. The data supports the premise that the labor sector began softening in early 2024, rising from 3.7% in January 2024 to 4.1%-4.2% for the second half of the year.

Another indicator of the health of the job market is weekly initial claims for jobless benefits. For the past six months weekly claims have averaged 228,000. However, in early June claims rose to their highest level in eight months to 250,000, but have since fallen four consecutive weeks to 223,000 for the last week of June. Another data point is continuing claims. These are people who have not yet found a job and are requesting benefits for another week. This number has been trending higher over the last couple of months. From December 2024 to mid-April 2025, continuing claims averaged 1.86 million. Since then, continuing claims have averaged 1.9 million. This implies it may be taking longer to find a job. It’s too early to suggest we are at the forefront of a sustained increase in unemployment, but it appears we are in a period of weaker employment.

While the increase in unemployment is somewhat concerning, the Fed believes the economy is near full employment despite the gradual rise in the jobless rate. For perspective, the unemployment rate over the past 20 and 30 years has averaged 5.8% and 5.5%, respectively.

Jobs, Unemployment and Hourly Earnings

Source: Bureau of Labor Statistics.

Gross Domestic Product

Real Gross Domestic Product (GDP) shrank by -0.5% for Q1 2025 largely due to a surge in imports as businesses scrambled to secure inventory ahead of an expected expansion in tariffs. (The ten-year average for first quarter growth is 1.7%.) Consumer spending slowed to 0.5% following 4% growth in Q4 2024, the strongest expansion in spending in eight quarters. We also saw an increase in business spending while housing and government spending contracted. Experts expect the noise from the surge in imports to unwind during Q2 with forecasts from the New York Federal Reserve projecting growth of 1.7% and the Atlanta Fed expecting activity to expand by 2.5%. For the second half of the year, look for GDP growth to expand at a modest pace with consumer and business spending fueling growth while government spending wanes. An increase in the inventory of existing homes for sale may cause some sellers to give more concessions to prospective buyers, which may spur sales and provide a positive contribution to GDP from the housing sector.

Gross Domestic Product .jpg?sfvrsn=6cec9ad_1)

Source: Bureau of Economic Analysis.

Inflation

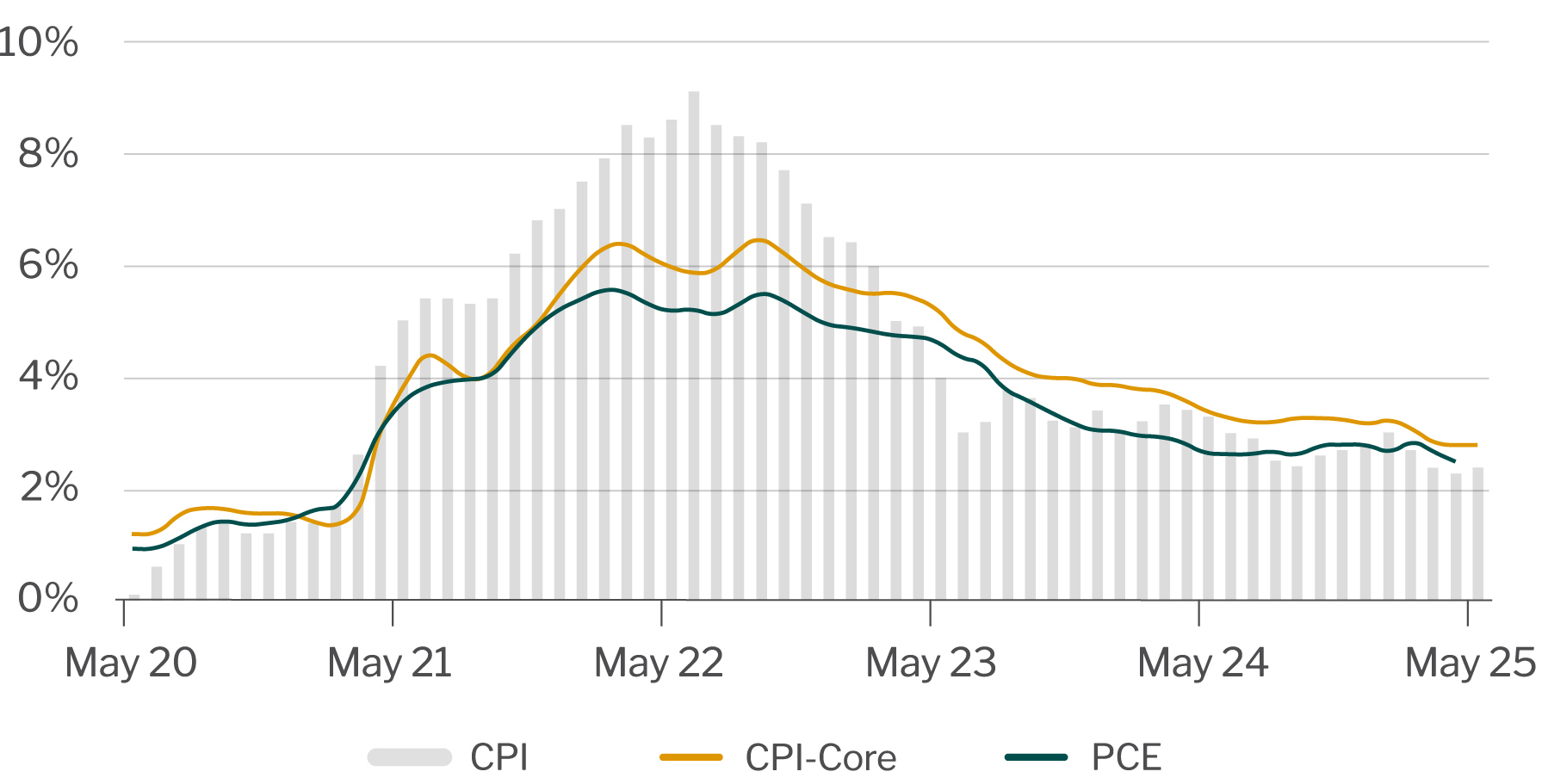

Accelerating inflation remains a concern for consumers and the financial markets. For May, prices increased 0.1% following an increase of 0.2% in April and a -0.1% decline in March. This suggests we've yet to see the impact on consumer prices related to the implementation of tariffs by the Trump Administration. However, inflation is expected to move higher over the next few months on recent increases in oil prices, which likely translates to higher gas prices, due to fighting in the Middle East and the basis effect of calculating the year-over-year rate of inflation. This increase in inflation is not expected to alter the path of policy rates indicated by recent comments from Federal Reserve officials.

Year-over-year consumer inflation is running at 2.4% as of May. We may see the Consumer Price Index increase to the 3.0%-3.5% level in the coming months, but then trend lower during 2026 as activity related to tariffs and geopolitical risks subsides. If inflation does not cool in 2026, the Fed may be forced to tighten policy rates to bring inflation under control.

Consumer Price Index

Source: U.S. Bureau of Labor Statistics. U.S. Bureau of Economic Analysis

Return to Industry Insights home page

IN THIS SECTION

![]()

.jpg?Status=Master&sfvrsn=68087301_1 "My project-1 (26)")

Economic headlines, data and trends

Monthly economic trends, data and major industry headlines.

Learn more