Spotlight: Crop acreage outlook

Many U.S. crops are facing profitability challenges in 2026. While prices for several major commodities are expected to improve slightly, elevated production costs will likely continue to erode much of those gains. As a result, spring planting decisions are increasingly driven by margin preservation. This is contributing to a shifting U.S. crop acreage mix.

The five largest U.S. crops by acreage, from highest to lowest, are corn, soybeans, hay, wheat and cotton. This Spotlight addresses corn, soybeans, and cotton. Please see the individual hay and wheat reports within this Monthly Market Update for detailed outlooks.

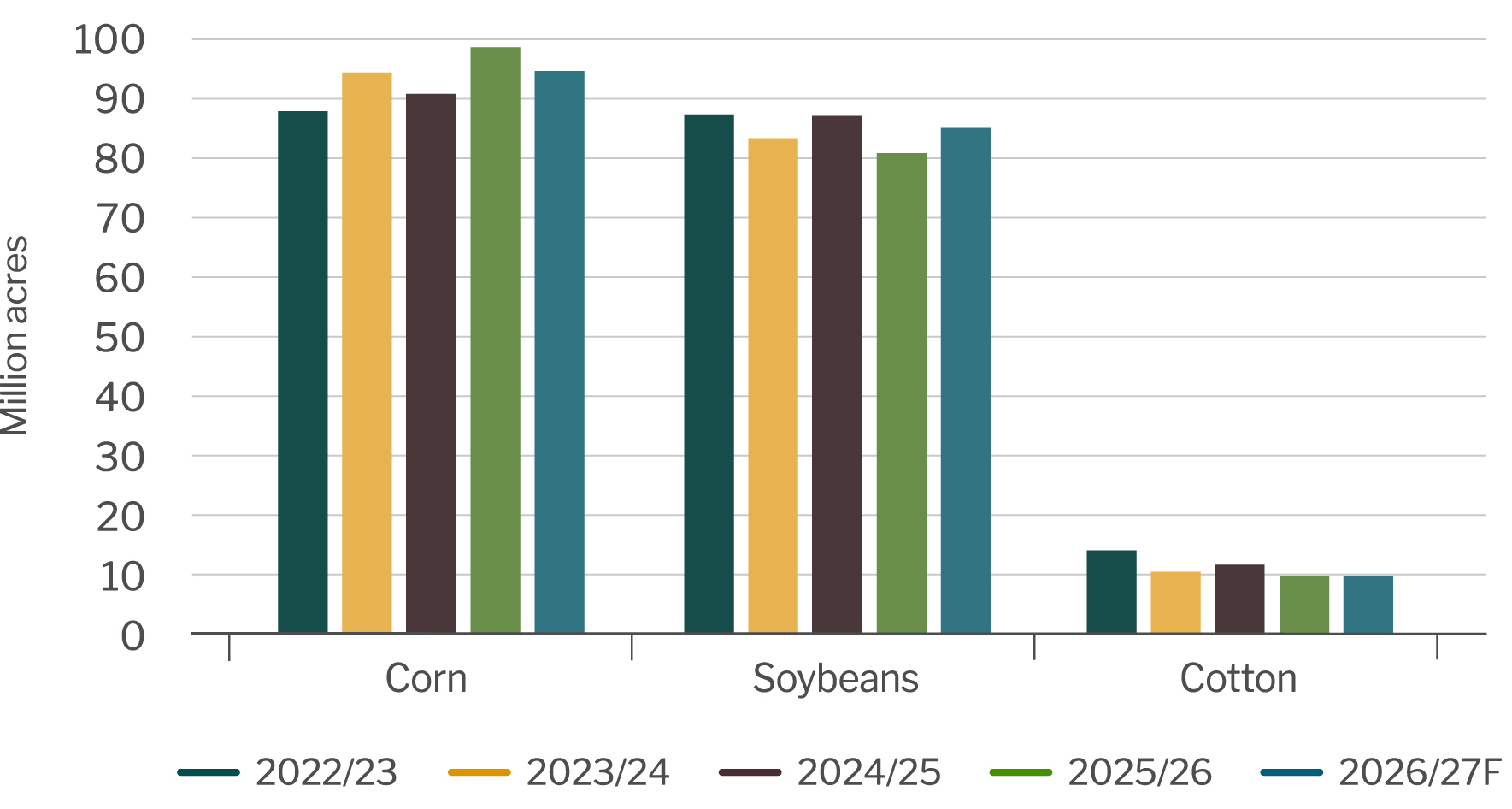

Planted acres by commodity

Source: USDA.

Corn

USDA projects U.S. corn planted acreage at 94.0 million acres in 2026, down 4.8 million acres from the previous year, reflecting continued margin pressure. While the season-average corn price for the 2026 crop is forecast to rise 10 cents to $4.20 per bushel, prices remain well below estimated breakeven levels of $5.01 per bushel, limiting corn’s ability to retain acreage.

Lower planted acreage is expected to reduce total production, tightening supplies. Corn exports are also forecast to decline by 200 million bushels to 3.1 billion, as increased supplies from South America are expected to reduce the U.S. share of global trade. Feed and residual use is also expected to soften slightly as the prospect of tighter supplies and higher prices temper demand.

Soybeans

Soybean acreage is projected to increase to 85.0 million acres in 2026, up 3.8 million acres from the previous year, with many acres shifting out of corn. The increase reflects lower input requirements, particularly for nitrogen fertilizer, which improves soybean competitiveness in a high-cost production environment.

The season average farm price for soybeans is projected at $10.30 per bushel in 2026, still well below the average cost of production, estimated at just over $12.00 per bushel. Soybean demand remains supported by steady global oilseed consumption and expanding domestic crush capacity, driven by growing biofuel demand for soybean oil. Biofuel demand continues to be reinforced by Renewable Fuel Standard and Low Carbon Fuel Standard programs. Soybean oil prices are forecast to increase 5 cents per pound to 58 cents per pound, supporting crush margins.

Export prospects remain a key uncertainty. While halted shipments to China have resumed, modest and inconsistent purchases have weighed heavily on the market. A trade agreement committing China to purchase at least 25 million metric tons annually from 2026 through 2028 is expected to support exports. However, narrowing price spreads with Brazil may temper gains in China and other export markets.

Cotton

U.S. cotton acreage is forecast to increase slightly to 9.4 million acres in 2026. This modest increase is largely driven by a rebound in Texas cotton acreage following historically low plantings in 2025. The season average farm price for upland cotton is forecast at 63 cents per pound, up 3 cents from the prior year, supported by slightly higher global cotton consumption and lower U.S. and world ending stocks. Despite the improvement, prices remain below breakeven levels for many producers.

Bottom Line

USDA’s outlook suggests many crops will continue to operate near or below breakeven levels in 2026, with crop insurance programs likely helping to offset some financial shortfalls. While corn and soybeans continue to dominate the acreage landscape, smaller shifts among secondary crops reflect ongoing efforts by producers to manage costs and risk as the growing season approaches.

Return to Industry Insights home page

IN THIS SECTION

![]()

.jpg?sfvrsn=68087301_1 "My project-1 (26)")

Economic headlines, data and trends

Monthly economic trends, data and major industry headlines.

Learn more