Land values - August 2025

Executive summary

The last six months have seen a continuation of land value trends across the West. Land values are generally stable; however, declines have been observed in parts of California, Idaho, Oregon and Washington primarily for the following reasons:

- California - Water supply constraints and depressed prices for certain fruit and nut crops, including table grapes, wine grapes, almonds and walnuts.

- Idaho and Oregon - Limited availability of high-quality properties, as opposed to falling demand.

- Washington - Falling prices for certain permanent plantings, including uncontracted wine grapes, apples (on low-productive properties) and hops, and limited availability of high-quality properties. These commodity sectors show decreased buyer interest and/or lower land values due to lower product prices and water supply concerns.

Persistently elevated interest rates and changing regulations continue to pressure demand across the West. Even where values are increasing, they are doing so at a slower rate. Property inventories for sale are increasing in California and Arizona but remain limited across the Northwest. Local operators, absentee operators, institutional investors and developers are active in the marketplace; however, development acquisitions have decreased primarily due to elevated financing costs. Some areas are reporting longer listing times and decreases in listing prices, though final sales prices indicate generally stable values.

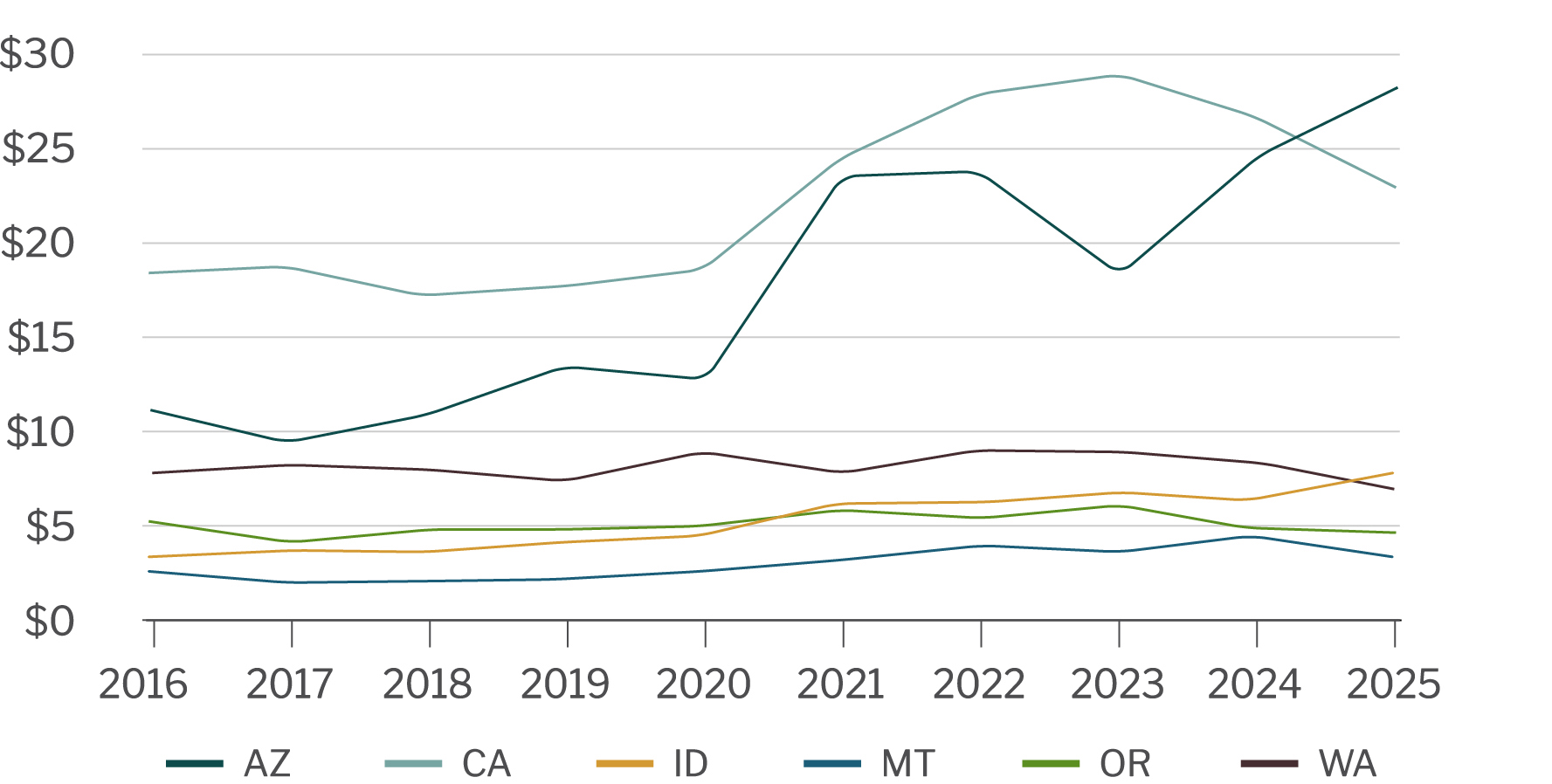

Average land values, thousands of dollars per acre

Source: AgWest’s proprietary sales database. Industrial, commercial, residential and site sales excluded. Data represents a 12-month rolling average. Data collection lags about six months and is subject to change. Recent changes in methodology have led to slight changes in values from the previous Land Values Report.

Average land values, thousands of dollars per acre

.jpg?sfvrsn=e7e07f08_1)

Source: AgWest’s proprietary sales database. Industrial, commercial, residential, and site sales excluded. Data represents a 12-month rolling average. Data collection lags about six months and is subject to change. Recent changes in methodology have led to slight changes in values from the previous Land Values Report.

Land value considerations

The implications of foreign land ownership extend beyond the figures, raising questions about policies, resource allocation, and security. Here are three key impacts to consider:

- Interest rates – Relatively high interest rates were a frequently reported deterrent to land acquisition. More instances of creative financing, such as owner-carried notes, have been reported.

- Rural residential/recreational – Most rural residential and recreational markets continue to cool, largely due to high interest rates. Longer listing times are becoming more common and prices appear to be stabilizing.

- Availability – Inventories of agricultural land are low in much of AgWest’s territory, which continues to bolster values despite elevated interest rates. A notable exception to this trend is in portions of California and central Washington, where broker reports and AgWest’s internal market data indicate supply is outpacing demand.

- Farm income/commodity prices – The relationship between land values and commodity prices in recent years has been weak as many perceive land as a stable, long-term investment. However, this relationship appears to be getting stronger in areas such as central Washington and California’s Central Valley as certain commodity prices are depressed.

- Drought – Drought conditions have returned to much of AgWest’s territory in 2025, with several portions of all chartered states showing severe to extreme drought. Precipitation levels are mixed throughout the West. The far north of California, much of Oregon, central Montana and western Idaho have experienced at or above median precipitation levels, while the rest of the territory is generally showing below median precipitation levels, particularly in Arizona. Refer to our Quarterly Drought and Water Update for more detailed information.

Arizona

- Agricultural cropland prices are stable to slightly increasing in the Greater Yuma Area, with some evidence of an increasing trend in the Yuma Mesa Area, although market activity has slowed. Farmers are not actively seeking land to purchase, although existing tenants will often decide to buy a farm offered for sale. Investor activity has slowed due to water concerns and elevated interest rates.

- Land values in southeast and central Arizona remain stable, with overall light market activity. Agricultural land surrounding the Phoenix Metropolitan Area is often purchased by investors due to consistent population growth, although investor activity has recently slowed due to elevated interest rates and long-term water supply concerns. Recently enacted “Ag-to-Urban” water right conversion policies may increase developer demand, but the impact cannot be measured at this time.

- Sales activities among dairy properties is slow. Extended listing periods are a possible indication of a softening market. Limited recent data indicates values and lease rates are stable.

- Colorado River states are embroiled in contentious negotiations over how to re-allocate scarce water as the Colorado River Compact expires in 2026. There is evidence of some progress, with Upper and Lower Basin states coalescing around a framework to allocate water based on “natural flows” (as if unimpeded by dams), although the technical details will likely prove thorny.

- Drought and poor Colorado River conditions in recent years have led to reduced Central Arizona Project deliveries and increased water rates for irrigation districts in Central Arizona and Pinal County.

- Market activity is cooling in rural Arizona, particularly in Cochise and Graham Counties amid concerns over declining groundwater levels and expanding groundwater regulations.

- Most participants in the pecan industry expect the market for average to good quality orchards to remain stable; however, low pecan prices and higher interest rates may slow sales activity and long-term water supply is questionable.

- Pistachio orchards are rarely offered for sale due to high profitability and ownership concentration in the industry, keeping pistachio orchard values relatively high, though long-term water supply is questionable.

California

- Access to water is the primary driver of agricultural land values in the San Joaquin Valley, with buyers preferring properties with access to multiple sources of water. Secondary drivers impacting land values include elevated interest rates and falling commodity prices.

- The unfolding implementation of the Sustainable Groundwater Management Act (SGMA) and related pumping restrictions has led to decreases in underlying land value across much of the San Joaquin Valley, particularly in those areas which lack access to surface water deliveries and/or don’t have a regulatory plan approved by the State Department of Water Resources. Greater clarity in the coming months should help to realign buyer and seller expectations.

- Despite some recent improvement, lower commodity prices have hurt land values in the San Joaquin Valley, notably among almond, walnut and table grape properties. This is also true of nut orchard values in the Sacramento Valley. Orchard contributory values have fallen precipitously (pistachio orchards show some resilience). Undesirable orchards are seen as a detriment, sometimes leading to purchases at open land value less removal cost. There is some evidence that the bottom may have been reached as low prices are now attracting buyers who were previously risk averse.

- Listing times across the Central Valley are stable to increasing as supply outpaces demand, a trend that has been compounded by the liquidation of multiple large vertically integrated grower/packer operations and agricultural investor groups. As a result, tens of thousands of additional acres are on the market.

- Demand for dairy facilities is decreasing due to weak domestic markets. The buyer pool is limited and prefers newer, more efficient facilities. Less efficient facilities, such as open lot corrals, are typically redeveloped into feed cropland or used as heifer facilities after purchase.

- Land values in the Sacramento Valley stabilized following gains in tree nut price over the last year. Cling peach orchard values are stable to strong, while prune orchards show some decline in value. Rice ground values are stronger in areas where surface water supplies are more reliable.

- Premium wine grape vineyards in the Central Coast are seeing reduced demand and declining values due to a persistent lack of wine demand. Vineyards located in western Paso Robles remain strong due to their wine’s strong reputation, favorable growing conditions and a larger buyer pool.

- The supply of irrigated cropland capable of vegetable and strawberry production on the Central Coast is very limited and in high demand, particularly in the Santa Maria Valley, which benefits from high quality soils and a relatively stable long-term water supply.

- Rangeland values are stable. Properties are usually directly marketed to a well-known buyer/lessee pool and typically sell quickly, keeping values elevated.

- Imperial Valley land values are stable with some evidence of slight decline, while market activity is slower due to high interest rates, decreased commodity prices and trade disputes. Historically this region appealed to investors seeking water security. This trend has dissipated in recent years and local growers and operators now make up most of the market participation.

Idaho

- Agricultural land values in Idaho remain stable to slightly increasing when compared with previous years. Demand for good quality agricultural ground continues to exceed supply, which helps buoy values.

- An agreement was reached in November 2024 between the Idaho Department of Water Resources (DWR) and several groundwater districts to avoid curtailments in the Eastern Snake Plain Aquifer. The agreement will be reviewed every four years. Surface water users will benefit from groundwater users adhering to mitigation and conservation requirements, while groundwater users benefit from long-term water right protection. Had this agreement not been reached, 300,000 to 500,000 acres of farm ground could’ve lost a significant amount of their value.

- The recreational market has slowed from historic highs, and properties are seeing longer listing times. Prices in this sector are difficult to track as there is relatively little data. Relatively high interest rates have pushed some prospective buyers out of the market, but demand is still evident.

- The rural residential market is stable, with limited supply creating upward pressure on values and elevated interest rates creating downward pressure on values. Prices are leveling off and listing times are increasing, but properties still sell in a reasonable timeframe.

Montana

- Much of Montana received median to above median snow by the historical peak day of April 14 in 2025, providing for adequate irrigation in most areas. Overall, agricultural land sales are stable to increasing throughout the state, primarily for higher quality production properties, which are limited in inventory.

- Demand for recreational ranch properties remains strong, particularly those with high amenities (recreational streams and ponds, good habitat for wildlife, access to public land, etc.). The TV show Yellowstone, which romanticizes ranch life in Montana, continues to drive demand from outside buyers for some properties, often referred to as the “Yellowstone Effect.” Lower-amenity recreational properties are starting to linger on the market longer with some seeing price decreases.

- Other good-quality agricultural real estate outside of ranching properties continues to be in high demand. Demand for lower-quality agricultural properties has softened, with longer listing times reported.

- Production agriculture still drives land values in many parts of the state, with many transactions taking place privately between landlords and tenants or between neighbors.

- Demand for rural residential properties has cooled from previous highs, due primarily to interest rates. Rural residential properties are seeing longer listing times, with some evidence of seller expectations exceeding buyer expectations.

Oregon

- Demand for good quality agricultural properties outpaces inventory throughout most of the region, except in parts of Central Oregon, where inventory appears to exceed demand. Lower quality agricultural properties have an increased risk of softening prices. Marketing times are generally increasing.

- Although demand continues to be strong for most property types, particularly from large operators, buyers are generally careful to ensure properties fit well within their existing operations. Investor and out-of-state buyer interest is mixed across the state.

- Elevated interest rates have led to a drop-off in demand and longer listing times of recreational properties. Evidence provided by the limited number of sales in this market segment suggests a possible downturn in the value of recreational properties.

- Demand for rural residential properties varies depending on location but a lack of inventory is generally keeping supply below demand, propping up values. Due to continued high interest rates, however, prices have leveled off from previous highs and longer listing times are common.

- There are some localized areas around Burns, Redmond and Klamath Falls with irrigation water concerns due to historic drought/water table issues and/or environmental concerns. This may be leading to longer marketing times as buyers hesitate.

- Catastrophic wildfires in multiple areas of Oregon during 2024 will result in widespread operational challenges over the next several years for affected producers and will likely impact availability of grass/pasture leases.

Washington

- Irrigated and dry cropland values are holding stable or increasing throughout the state. Many permanent planting properties, particularly hops, uncontracted grapes and marginal apple orchards in central Washington are seeing longer listing times and weakening values.

- The Columbia Basin Irrigation Project is gaining nationwide attention, attracting out-of-area buyers looking for investment in quality farm ground with reliable water availability and a diversity of crop options.

- Longer listing times and discounts have been seen on marginal quality orchards over the last several months as supply outpaces demand. Demand for orchards has softened, and those with long-term inefficiencies and out-of-date varietals are experiencing the largest decreases in values.

- In areas where a recreational market exists, few sales have occurred, and extended listing times are common.

- Rental rates are beginning to soften in some areas, which may suggest land prices will follow if commodity prices remain depressed.

- The rural residential market has slowed significantly due to elevated interest rates; however, demand still exists for good-quality properties outside of larger communities. There is upward pressure on farmland surrounding population centers.

Share your feedback! Click here to complete a two-minute survey about this report.

About AgWest Farm Credit Appraisal Services

AgWest appraisers provide appraisal services on rural properties throughout the West. The Appraisal Services team continually researches sales and tracks market data throughout Arizona, California, Idaho, Montana, Oregon and Washington. They compile the market data and analyze it using a central database.

This report provides a high-level look at trends and market characteristics and does not provide details for specific areas or land types. The report should not be used to identify the value of a specific property. This information is limited only to an analysis of trends in identified land values within the geographic area served by AgWest Farm Credit.

Learn more

For more information or to share your thoughts and opinions, contact the Business Management Center at 866.552.9193 or CustomerFeedback@AgWestFC.com.

To receive email notifications about western and global agricultural and economic perspectives, trends, programs, events, webinars and articles, visit www.AgWestFC.com/subscribe.

Return to Customer Stories home page.